Kevin Warsh Fed Policy Shock:

Could Higher Rates Pressure AI Stocks

Small Fed · balance-sheet reduction · inflation pressure · AI stock rotation · HBM supply chain

Kevin Warsh Fed policy is now one of the most important macro variables for global markets. Reuters reported that Kevin Warsh officially took the oath as Federal Reserve Chair and FOMC Chair on May 22, 2026. The market is no longer asking whether Warsh will lead the Fed. The real question is whether his preference for a smaller Fed balance sheet, persistent inflation pressure, and rising long-term yields could trigger a new round of valuation pressure on AI stocks and Korean semiconductor exporters.

Kevin Warsh Fed Policy: A Smaller Balance Sheet Could Keep Long-Term Yields High

Kevin Warsh is difficult to classify as simply dovish or hawkish. On one side, some policy interpretations suggest that he may prefer lower short-term rates to support households, small businesses, and productive investment. On the other side, he has long favored reducing the size of the Federal Reserve’s balance sheet.

That combination matters. A smaller Fed balance sheet can reduce market liquidity and put upward pressure on long-term yields if private investors must absorb more Treasury and mortgage-backed securities. In other words, short-term rates could move lower while long-term rates remain high or even rise.

Rate Hike Fear Returns as CPI and PPI Reaccelerate

The biggest constraint on any dovish interpretation of Warsh is inflation. The U.S. Bureau of Labor Statistics reported that the CPI rose 3.8% year over year in April 2026. The PPI for final demand rose 6.0% over the 12 months ended in April. Those numbers are not compatible with an easy, immediate rate-cut narrative.

This is why the market has started to price a more uncomfortable possibility: if inflation remains sticky and energy prices keep pressure on consumer and producer costs, the Fed may be forced to stay restrictive for longer. In the most stressful scenario, rate-hike fear can return even under a Fed chair who once argued for lower rates.

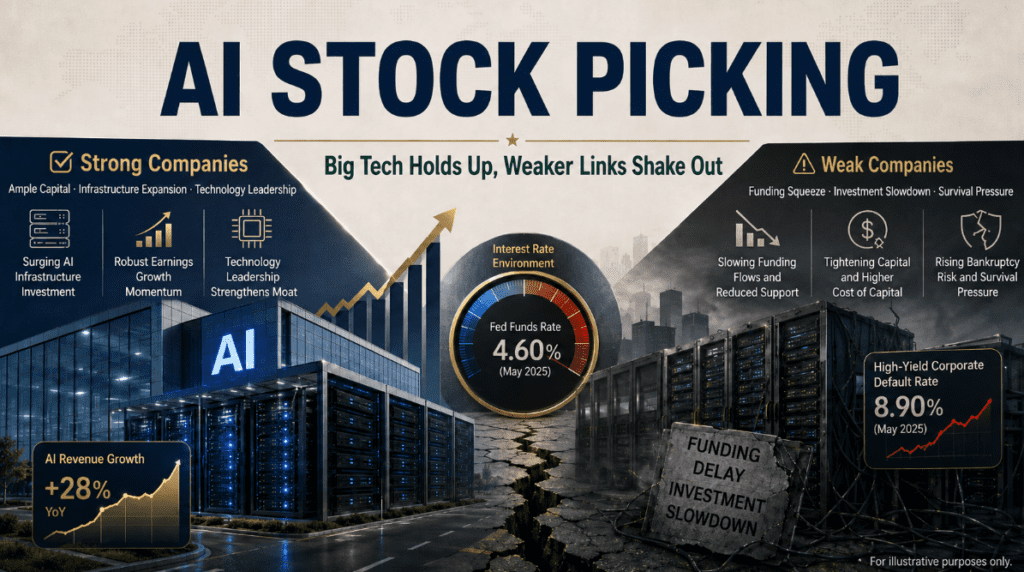

AI Is Still Strong, But Higher Rates Will Separate Winners From Hope Stocks

Nvidia’s latest earnings show that the AI infrastructure cycle remains powerful. AP reported that Nvidia’s revenue jumped 85% to $81.62 billion, and CEO Jensen Huang described the buildout of AI factories as the largest infrastructure expansion in human history.

But a high-rate environment changes how investors value AI. Mega-cap cloud platforms and AI chip leaders can justify spending because capex is turning into revenue. Smaller AI infrastructure suppliers, data-center intermediaries, and companies funded mainly by future expectations may struggle as financing costs rise.

| AI Group | Strength | High-Rate Risk |

|---|---|---|

| Tier 1 winners | Nvidia, hyperscalers, cash-rich platforms | Lower, because revenue conversion is visible |

| Tier 2 hopefuls | Data-center suppliers, smaller component names, funded growth stories | Higher, because financing costs matter more |

Kevin Warsh Fed Policy: This Is Not a Simple Rate-Cut Market

The market wants a clean story: new Fed chair, lower rates, higher stocks. But the Warsh regime may be more complicated. A smaller balance sheet can support a tighter long-end liquidity environment, while CPI and PPI inflation make immediate rate cuts harder to justify.

Final view: AI is not over. But the easy phase of the AI trade may be over. The next phase is about earnings, cash flow, balance-sheet strength, and real AI infrastructure revenue.

- Reuters — Warsh elected chair of U.S. Fed’s rate-setting committee

- U.S. Bureau of Labor Statistics — April 2026 CPI Summary

- U.S. Bureau of Labor Statistics — April 2026 Producer Price Index

- AP News — Nvidia Q1 results and AI chip demand

- Charles Schwab — Warsh balance sheet analysis

- BNP Paribas — Kevin Warsh policy implications

- Reuters — SK Hynix and AI memory demand

⚠️ Disclaimer: This article is for informational and educational purposes only and does not constitute financial or investment advice. Market conditions can change quickly. Always conduct your own research before making investment decisions.