Iran Shockingly Proposes Temporary Deal — Microsoft Restructures OpenAI Partnership, Oil Surges

By Felixsr · Economics · 7 min read

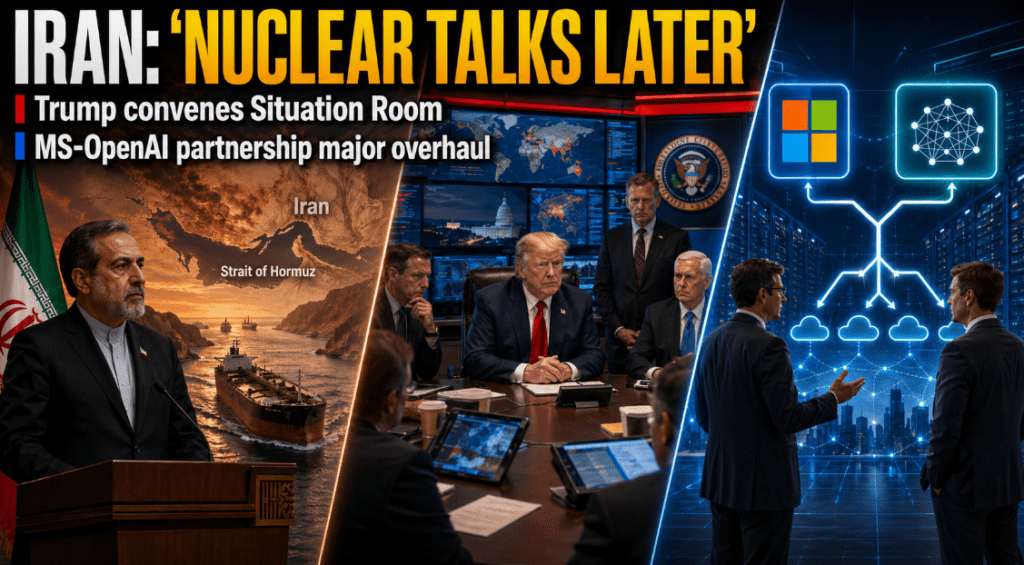

April 27 opens with a shockingly busy pre-market: Iran has proposed a temporary interim deal — open Hormuz first, discuss nuclear terms later — in the most concrete diplomatic move yet. Microsoft and OpenAI quietly restructured their partnership, removing Microsoft’s IP exclusivity while freeing OpenAI to serve other cloud providers. Oil is rising on Iran negotiation uncertainty, and a third assassination attempt against Trump over the weekend has triggered a major White House security review.

Iran Shockingly Proposes Interim Deal on April 27 — Open Hormuz First, Nuclear Later

In the most significant diplomatic development since talks began, Iran has formally proposed a phased interim deal: open the Strait of Hormuz to commercial shipping first, then negotiate the nuclear suspension terms separately. Iran’s Foreign Minister delivered the proposal, stating the US has “failed to achieve its goals” and calling for negotiations on Iran’s own terms.

The White House has not formally responded as of market open. Trump convened a National Security Council meeting over the weekend to evaluate whether to resume bombing after the ceasefire — a signal that the US position remains firm on the nuclear-first sequencing. The contradiction between Iran’s Hormuz-first proposal and America’s nuclear-first demand is the key sticking point on April 27.

“The United States has failed to achieve its objectives. We are prepared to negotiate — but on the basis of mutual respect, not under the pressure of threats and ultimatums.”

Microsoft and OpenAI Quietly Restructure — IP Monopoly Ends, Multi-Cloud Era Begins

In a major structural shift announced on April 27, Microsoft and OpenAI have revised their partnership agreement. The key change: Microsoft gives up its exclusive IP licensing rights over OpenAI’s technology in exchange for a revised revenue-sharing structure. In return, OpenAI gains the freedom to deploy its products on non-Azure cloud infrastructure — ending Microsoft’s lock on OpenAI’s cloud dependency.

This is a significant strategic realignment. Microsoft retains its position as OpenAI’s primary cloud partner and major shareholder — but loses the exclusivity moat that had made the relationship uniquely valuable. For OpenAI, the flexibility to serve customers on AWS, Google Cloud, or Oracle infrastructure removes a major enterprise sales obstacle heading into its IPO.

| Before Restructure | After Restructure |

|---|---|

| Microsoft holds exclusive IP rights | IP exclusivity removed |

| OpenAI locked to Azure cloud only | OpenAI can use any cloud provider |

| Microsoft = primary cloud + IP holder | Microsoft = primary cloud + major shareholder only |

| Revenue structure: fixed | Revenue structure: revised, OpenAI gets more flexibility |

Third Trump Assassination Attempt Over the Weekend — White House Security Overhaul Ordered

The White House confirmed over the weekend that a third assassination attempt against President Trump occurred — making it the third serious attempt in the past two years. The press secretary called it historically unprecedented: “No president in American history has faced this level of repeated, serious threats to their life.” Trump personally visited injured Secret Service agents and was described as calm throughout the incident.

In response, a major White House security review was ordered for this week — involving the Secret Service, DHS, and the NSC. The political dimension is also significant: Trump simultaneously called for Disney to fire its CEO Jimmy Kimmel, signaling he intends to remain fully engaged on multiple fronts despite the security threat.

April 27 Earnings Beats and Wall Street Calls to Watch Today

Earnings season continues at full pace on April 27 with several notable pre-market and after-hours results. Cadence Design Systems, Rambus, and Amkor Technology all beat on EPS and revenue. Meanwhile, Wall Street analysts are making aggressive calls — JPMorgan says the market selloff is a buying opportunity, Morgan Stanley recommends holding the barbell strategy, and Goldman Sachs raised its Q4 Brent crude forecast from $80 to $90.

| Stock / Institution | News | Direction |

|---|---|---|

| Cadence (CDNS) | EPS/revenue/margin beat — full-year revenue raised | ▲ Strong |

| Amkor (AMKR) | EPS/revenue beat — Q2 revenue outlook raised | ▲ |

| Oracle (ORCL) | Completes $16B data center financing round | ▲ |

| Google (GOOGL) | AI chips narrow cloud competitive gap vs rivals | ▲ |

| Qualcomm (QCOM) | Joins OpenAI smartphone development project | ▲ |

| Snap (SNAP) | Redburn upgrades to Buy — target $10 | ▲ |

| Marvell (MRVL) | Cancels contract with Fonet Technology | ▼ Watch |

| JPMorgan | “Market weakness is a buying opportunity” | ▲ Bullish signal |

April 27 Has 3 Moving Parts — Here’s How to Read Them Together

Today is genuinely complex. Three major stories are running simultaneously — and they pull markets in different directions.

Bottom line for April 27: Iran White House response + Big Tech earnings = the two variables that will define this week. Everything else is secondary noise.

“Earnings are driving returns — maintain the barbell strategy. Strong corporate results continue to provide a buffer against geopolitical uncertainty and energy price volatility.”

- Reuters — Iran proposes interim Hormuz-first deal framework ↗

- Bloomberg — Microsoft OpenAI partnership restructure details ↗

- CNBC — Trump assassination attempt #3, White House security review ↗

- Wall Street Journal — Goldman Sachs raises Brent Q4 forecast to $90 ↗

- Financial Times — Big Tech earnings week preview April 27 2026 ↗

- MarketWatch — JPMorgan: market weakness is a buying opportunity ↗

⚠️ Disclaimer: This post is for informational purposes only and does not constitute financial or investment advice. All data reflects market conditions on April 27, 2026. Always conduct your own research before making investment decisions.